Investor blogs and podcasts

In Kesko’s investor blogs and podcasts, Kesko’s management discusses topical issues relevant to investors and shareholders.

Recap of Kesko’s key events in Q2/2026

Kesko will publish its half-year financial report for 2026 on Wednesday, 22 July 2026, at around 8.00 am Finnish time. An English-language audiocast/teleconference for investors and analysts will be held at 9.00 am Finnish time and can be accessed here.

Below you'll find a recap of key news and events in the second quarter.

NEWS, FINANCIALS AND SHARES

-

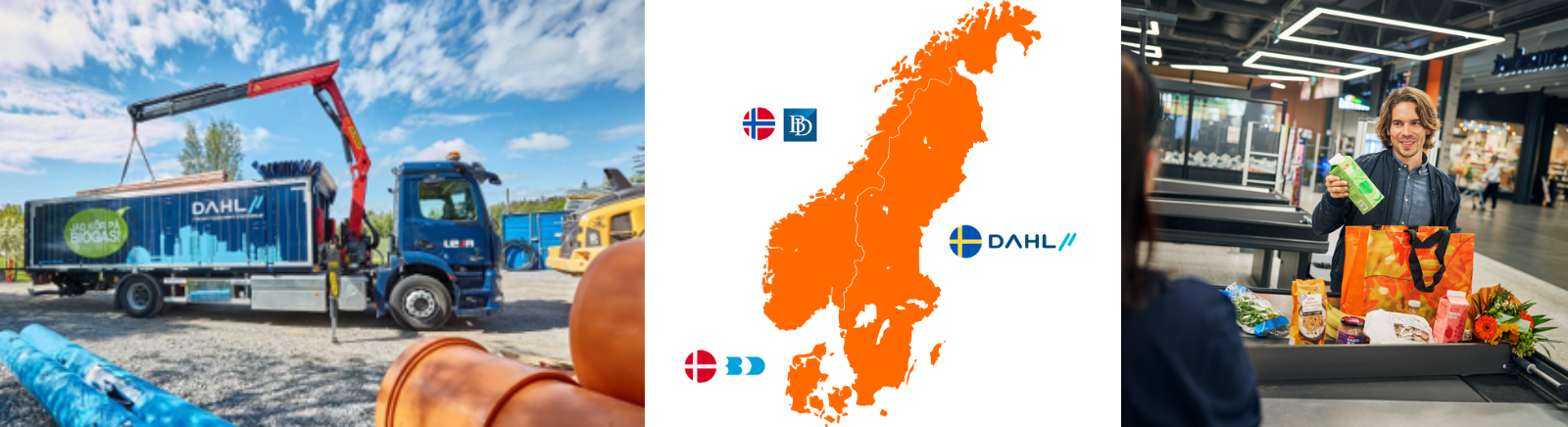

Kesko announced it will acquire the technical trade operator Dahl’s companies in Sweden, Norway and Denmark. The combined net sales of the companies to be acquired totalled nearly €2.1 billion in 2025. The largest transaction in Kesko’s history is set to expand Kesko’s reach in the HPAC and infrastructure construction businesses in Sweden, Norway and Denmark. The debt-free transaction price is €1,200 million excluding lease commitments (€1,518 million including lease commitments). The completion of the acquisition is subject to approval by competition authorities and is expected to take place by the start of 2027.

-

Shares:

-

Change in the holding of treasury shares (release 17 April)

-

Change in the holding of treasury shares. (release 30 April)

-

-

Presentation for Kesko’s investor roadshow meetings in Q2. (presentation)

SALES DEVELOPMENT

Sales figures for June will be released in mid-July.

GROCERY TRADE

-

K Group grocery stores gained market share every month between October last year and March 2026, and the positive momentum has continued. The gains in market share can be attributed to strategic investments made quality, prices and store network development, but they have not come at the expense of profitability. (investor blog post)

SUSTAINABILITY

-

Kesko was again included in the Dow Jones Best-in-Class World and Dow Jones Best-in-Class Europe sustainability indices (DJ BIC). Kesko was among the top five companies in its industry to be included in the DJ BIC World, receiving strong scores for e.g. Transparency & Reporting, Biodiversity, Water, Climate Strategy, and Human Rights. (release)

-

Kesko’s sustainability work in action. Sustainability work at Kesko is carried out across all divisions in various ways. Our investor blog post highlights recent progress made and plans under each the themes of Kesko’s sustainability strategy. (blog post)

Questions and answers about the Dahl acquisition

Kesko announced on Monday, 15 June 2026 that it has agreed to acquire the companies of leading Nordic technical trade operator Dahl in Sweden, Norway and Denmark. Below you will find some questions and answers concerning the transaction.

FINANCIAL FIGURES AND IMPACT

What is the operating profit for the companies to be acquired?

-

We and the seller have agreed not to disclose operating profit figures for the companies to be acquired. All three companies are profitable, with the biggest one in Sweden being the most profitable.

How does Dahl’s operating margin compare to that of Kesko’s building and technical trade division? Dahl’s EBITDA of 7.1% is close to that of Kesko’s building and technical trade – how do you intend to increase value when the EBITDAs already align?

-

We have agreed with the seller that operating profit figures for the acquired businesses will not be disclosed.

-

When comparing the figures for Kesko and Dahl, it is worth noting that the figures for Kesko’s building and technical trade division also include building and home improvement trade. In technical trade, profitability is supported by a business model that relies less on, for example, the store network and more on high volumes, automated central warehouses and digital sales.

-

Dahl represents technical trade, just like Onninen in Kesko. In 2025, the operating margin for Kesko’s technical trade was 3.9% and in 2024 it was 4.0%, while the figures for building and home improvement trade were 3.0% (2025) and 2.7 % (2024). In Finland, Onninen’s operating margin was 5.1% in 2025 and 6.1% in 2024.

-

Dahl is 100% technical trade, and its business is based on automated central warehouses, with a high share of digital sales. Dahl’s digital sales account for around 35% of sales and Onninen’s for 39%.

Why does Kesko pursue this deal at a higher multiple than prior acquisitions?

-

This is a very rare opportunity. Dahl is in the heart of our growth strategy for building and technical trade. It is a leading technical trade distributor in HPAC in the Nordics and from Kesko’s perspective the strategic fit is extraordinary.

-

Valuation-wise we have considered Dahl’s long-term performance over the current low cycle and also future potential with strong market positions in the growing technical trade market. There’s also meaningful upside from operational perspective. On this basis, the deal is strategically compelling and financially accretive longer term.

What is the expected impact of the acquisition on earnings per share (EPS)?

-

The impact on EPS will depend on the final structure of the long-term financing package. At this stage, the company does not intend to provide specific guidance on the immediate EPS impact of the transaction. Over the medium to long-term, however, the acquisition is expected to be EPS accretive, supported by disciplined strategy execution, as well as increased scale and market position.

Will the acquisition impact Kesko’s dividends?

-

It will not, Kesko's dividend policy aims to distribute a dividend of some 60-100% of its comparable earnings per share, taking into account the company’s financial position and strategy.

What is the interest rate for financing the acquisition?

-

In the bridge financing, the rate is close to Kesko’s current level. The interest for future refinancing depends also on market conditions, but our aim is to keep it at the same level as it would be without this kind of deal. At the moment, we are at 3.3 -3.5 % on average in this type of financing.

How will the equity component be raised and when?

-

The plan is for the equity component of the financing to be implemented through a share issue estimated at approximately €500–700 million. No decision has been made regarding the form of the equity issue, while the timing will be subject to securing the acquisition and market conditions.

-

Kesko will assess financing alternatives at the later stage taking into account balance sheet considerations, market conditions and the interest of its shareholders.

-

Kesko’s Board of Directors, or the General Meeting if necessary, will make a separate decision regarding the details of the issue at a later date. The Board has been authorised by Geneal Meeting to decide on the issuance of a maximum of 33,000,000 Kesko B shares.

DAHL AND ITS IMPACT ON KESKO’S OPERATIONS

How many stores does Dahl have in Sweden, Norway and Denmark?

-

There are nearly 190 stores in total: 80 in Sweden, 54 in Norway and 53 in Denmark.

How has Dahl’s Nordic business developed this year versus 2025? Can you see signs of the market cycle turning

-

We cannot disclose Dahl’s latest figures, but overall we can see that the market is gradually improving. New residential starts are still at the lower level, but we see that activity is going the right direction. It is worth noting that renovation building accounts for approximately half of Dahl’s sales, and the stable infrastructure construction business accounts for approximately one-third. We see a lot of opportunities in these businesses.

What kinds of synergies do you expect to obtain?

-

We expect to see synergies in purchasing and own brand products, as well as in IT, for example. This is primarily a strategic acquisition, and synergies are not the main driver.

-

In HPAC products, our sales volumes will close to triple from one €1 billion nearly €3 billion.

-

We will leverage synergies between Dahl and Kesko businesses in different countries to drive, for example, a higher share in private labels. Dahl is already well managed – our priorities are to retain the heritage and customer relationships. This is not a headcount-reduction or cost-slashing case.

What will be Kesko’s market position and market shares following the acquisition?

-

We are already the market leader in Finland with a market share of over 40%. Following the acquisition, we would be the market leader in Norway as well, with market share of some 40%, and #3 on the market in Sweden and Denmark, with market shares of 20% and below 20%, respectively.

The acquisition includes three central warehouses – are you anticipating investment needs related to those facilities?

-

We do not anticipate any immediate investment needs: the warehouse in Sweden is only a couple of years old, and the facilities in Norway and Sweden have been updated and have a high level of automation.

Do the lease agreements of the companies to be acquired differ in length from those on Kesko’s building and technical trade?

-

The lease agreements are aligned with those of Kesko.

-

What will happen to Dahl’s operations in Finland and the Baltics?

-

Kesko acquires Dahl businesses in Sweden, Norway and Denmark – we cannot comment on other operations on behalf of the seller. Kesko already has a strong market position in Finland and the Baltics.

How will the acquisition and building and technical trade becoming Kesko’s biggest division in terms of sales impact the grocery trade division and the car trade division?

-

The acquisition will not impact Kesko’s grocery trade and car trade divisions, which have their own effective strategies that we will continue to execute.

Kesko’s everyday sustainability work yields tangible results

Sustainability work at Kesko is carried out across all divisions in various ways. Our sustainability strategy focuses on the following key themes: climate and nature, value chain, our people, and good governance. In this blog post, we highlight recent progress and plans under each of these themes.

Theme: climate and nature

Reducing emissions

A key priority in our sustainability strategy is advancing Kesko’s emission targets. In January 2026, the international Science Based Targets initiative (SBTi) validated Kesko’s new near-term and long-term science-based emission reduction targets.

“We have a plan extending to 2034 to reduce emissions from our own operations, and we are proceeding according to the plan. Key measures include electrifying logistics and switching to biofuels, improving energy efficiency, and the use of renewable energy. We are also currently preparing a plan to reduce emissions across the value chain. Most of Kesko’s value chain emissions arise over the lifecycle of the products we buy and sell, from production to use and end-of-life treatment. This means cutting value chain emissions will require new measures, and all suppliers will need to be encouraged to join the effort,” says Noomi Jägerhorn, Kesko’s Vice President of Sustainability.

Read more about our emission targets and the plan for emissions from our own operations

Assessing nature impacts

During 2025, Kesko prepared preliminary plans to mitigate biodiversity-related impacts in its value chain. To build a better understanding of nature impacts in the value chain, we also launched a cooperation with an external partner to calculate the nature footprint of our private label products in the grocery trade.

Innovations in circular economy

Kesko and K Group promote the circular economy in many ways: in addition to sorting and recycling in our own operations, we can also encourage consumers to support the circular economy and change their everyday habits. For example, the Rinki eco take-back points located on our store premises make it convenient for customers to recycle while doing their shopping.

“Kesko and K Group stores are taking steps towards achieving the EU target of reducing the use of plastic carrier bags. We are also developing new circular economy solutions, such as the pioneering recycling model for wood packaging waste piloted last year, and the ongoing pilot of reusable take-away containers,” says Jägerhorn.

Read more about the circular economy

Theme: Value chain

Sourcing from near and far

Kesko has several sustainability policies guiding operations and sourcing. Over the past year, these policies have been updated to reflect, among other things, changes in sustainability regulation. Progress under each policy is described in more detail in a table at the bottom of each policy page.

The Pirkka Parhaat small supplier development programme is one example of how we aim to speed up access to store shelves for products from Finnish small food suppliers. Applications for the second programme are open until the end of June. As a result of the first programme, four products were added to our Pirkka Parhaat premium private label range in 2025.

Noomi Jägerhorn, Kesko's Vice President of Sustainability

Noomi Jägerhorn, Kesko's Vice President of Sustainability

A new product will be added to Kesko’s ‘Tracing our products’ website this year: “The website will soon provide our customers with information on the origin of our Pirkka Costa Rica coffee and its journey to our grocery stores. Coffee is one of our most popular products, which is why we want to give customers more information about where it comes from. Coffee production is also facing challenges, as climate change is making cultivation more difficult. We hope that in the coming years we will be able to provide even more detailed information on the origin of our products as data availability improves and technology develops,” says Jägerhorn.

Read more about our value chain and sourcing

Theme: Our people

Towards a more diverse workplace

Kesko’s goal is to increase the share of women in top management to 40% and in middle management to 45% by 2030. During autumn 2025 and the following winter, a women’s leadership incubator programme was organised for the second time together with Mothers in Business (MiB) ry.

“We’ve gotten excellent feedback for the incubator, and it is seen as a good way to support women’s career development. The next leadership programme aimed at women is scheduled to begin later this year,” says Jägerhorn.

Read more about Kesko’s diversity work

Theme: Good governance

New regulation tightening rules on green claims

Changes in sustainability regulation affect Kesko’s operations. One example of regulation that also affects consumers is the EU Empowering Consumers Directive (EmpCo), which affects companies’ marketing and communications and how they can talk about sustainability going forward. Instead of using general claims such as “sustainable” and “environmentally friendly”, companies will need to provide concrete, verified facts about products and services.

“At Kesko, we have been preparing for the legislation, which will start to apply from the end of September, by training our people and the K-retailers, informing our suppliers, and reviewing packaging and website texts. Our goal is to ensure that our products, communication and marketing continue to meet the requirements of the law,” says Jägerhorn.

More information on progress towards the key targets of our sustainability strategy can be found in Kesko’s Annual Report and on our sustainability pages

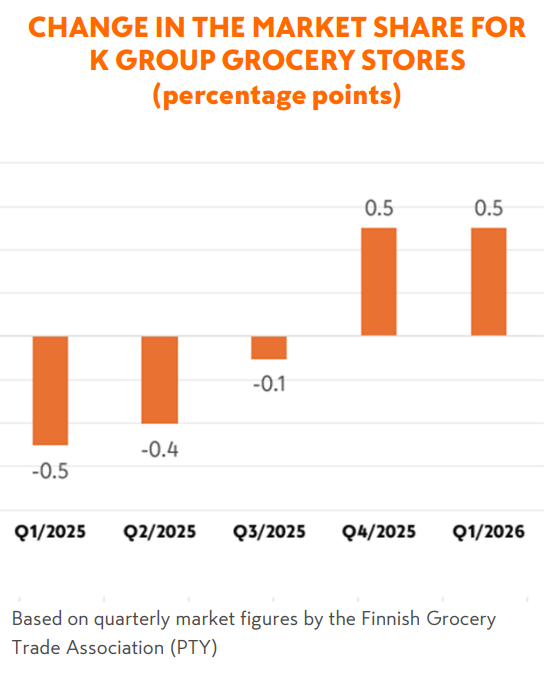

K Group grocery stores are gaining market share while maintaining good profitability

The market share for K Group grocery stores grew by 0.5 percentage points year-on-year in the first quarter of 2026 (source: Finnish Grocery Trade Association, PTY). After negative development in 2022-2024, K Group’s market share took a positive turn last summer, and between October and March we gained market share every month. The K-Citymarket chain gained market share in the hypermarket segment throughout last year. In Q4/2025 and Q1/2026, our other two grocery chains – K-Market and K-Supermarket – also gained market share in their respective segments (in year-on-year comparison). The total grocery market in Finland grew by 2.9% in Q1, while K Group’s grocery sales grew by 4.4%.

Strengthening market share was one of the main objectives set for Kesko’s grocery trade division when the Group strategy was updated in spring 2024. However, it was equally important to maintain good profitability despite efforts to boost market share, and the division’s operating margin target was set at “clearly above 6%”. In the first quarter of 2026, the division’s operating margin was strong at 6.5% (rolling 12 months) despite the market share gains achieved.

Investments in quality, prices and store network development contributing to market share growth

The positive development in market share can be attributed to the long-term strategic investments made in the price and quality levels of the stores as well as the development of the grocery store network.

Prices: The Finnish grocery trade market has been very price-driven in recent years, and price continues to be an important consideration for many customers. In January 2025, Kesko and K-retailers launched an extensive long-term price programme, cutting prices on more than 1,200 popular everyday staples in K Group grocery stores. Combined, Kesko and the retailers invested €50 million in the programme last year. In addition to the price programme, we have actively invested in campaigns as well as in targeted personal offers and benefits. The efforts have paid off, as customer flows in K Group grocery stores have grown. Average purchase is also up, and customers are not buying only the discounted products, but increasingly do their main weekly shop at our stores.

Quality: Raising the quality level of K Group grocery stores further involves a wide range of actions aiming to ensure suitable selections, good product availability, excellent customer service, reliable and useful digital services, and high quality products. In the current strategy period, special attention has been paid to certain key product categories, such as bread and fruit and vegetables. The implementation of store-specific business ideas, tailored to local demand and customer base, plays a crucial role in developing better stores. The business ideas can be implemented even more effectively with the help of new tools that utilise data and AI for easier selection and campaign management, thus freeing up store staff for more personal customer service.

Efforts to improve quality have paid off, as customer satisfaction grew clearly in all three K Group grocery chains in both Q4/2025 and Q1/2026. Demand for valuable and premium product categories, such as service counter items, fruit and vegetables and high-quality ready meals, has also grown.

New premium flower departments and the development of popular K-Ruoka digital services are examples of investments made in customer service and quality.

Store network: Having the right-sized stores situated in the right locations supports positive market share development. Kesko invests €200-250 million annually in the development of its grocery store network. In 2025, we opened 60 new or remodelled stores, including 2 new K-Citymarket hypermarkets. In 2026, we will open 25 new stores and remodel more than 60. Network development covers stores of all sizes, although growth in Finnish grocery trade in recent years has been the strongest in larger stores sizes, such as hypermarkets. In new store openings, our focus is especially on urban growth centres. Meanwhile, store remodelling often involves aspects such as updating refrigeration equipment to meet the requirements of tightening EU regulations.

Network development can also involve closing stores, which can have a negative market share impact in the short term. For example, the discontinuation of the Neste K chain in 2024 reduced the number of our stores by over 60. All together, network changes made by both K Group and its competitors had a negative impact on K Group’s market share in 2025, while in 2026, the impact is expected to be neutral. Network development efforts should gradually support our market share development in upcoming years.

President and CEO Rauhala: Strong sales and profit in all Kesko divisions in Q1

"In the first quarter of 2026, Kesko’s profit improved and net sales grew in all divisions. Kesko’s Q1 net sales totalled €3,029 million. Net sales grew by 4.6% in comparable terms year-on-year. Kesko’s comparable operating profit amounted to €102 million, and grew by €6.5 million. Cash flow from operating activities grew markedly stronger thanks, in particular, to good working capital management. All three divisions showed positive development even though the market remained relatively challenging. The crisis in the Middle East does not have a significant impact on Kesko’s operations in the short term, but a prolonged situation could result in weakened consumer confidence, purchasing power and corporate investments as well as higher costs.

In the grocery trade division, our long-term strategic efforts focused on quality, price, and the store site network yielded results. For the first time since the pandemic, the division saw growth on all three fronts: net sales, profit, and market share. Net sales for the division grew by €72 million and totalled €1,558 million. The comparable operating profit for the division totalled €78.4 million, up by €5.5 million. The market share for K Group grocery stores took an upturn in the summer of 2025, and the positive trend has continued in 2026: our grocery store chains all won over market share in Q1 in their respective size segments. K Group grocery sales grew by 4.4% against a total market growth of 2.9%. Customer flows and average purchase also grew. Although price plays a significant role in the grocery trade market, demand for quality products and services has increased. Net sales for the foodservice business decreased by 0.6%, but Kespro continued to gain market share.

In the building and technical trade division, net sales grew by €114 million and totalled €1,147 million. The division’s comparable operating profit amounted to €14.5 million, up by €2.8 million. Net sales for building and home improvement trade increased by 16.9% underpinned by acquisitions, or by 3.3% in comparable terms. K-Rauta’s comparable operating profit in Finland decreased slightly, but remained at a good level. In technical trade, comparable operating result improved in all operating countries, and net sales grew. In Finland, Onninen gained market share markedly in the first quarter. Gradual recovery in the construction cycle has continued in all our operating countries.

In the car trade division, net sales totalled €331 million. Net sales grew by €17 million year-on-year, driven in particular by used car sales. The comparable operating profit totalled €16.1 million, down by €1.8 million. The division gained market share in both new and used cars, and service sales increased. The order book for new cars grew due, in particular, to interesting new models. In sports trade, sales and profit grew and market share improved.

We repeat our profit guidance and estimate that the comparable operating profit for 2026 will amount to €650–750 million. We estimate that the operating environment, net sales and profit will improve in all divisions and all operating countries in 2026.

KEY FIGURES IN JANUARY-MARCH 2026:

-

Group net sales in January-March totalled €3,029.0 million (€2,827.7 million); reported net sales grew by 7.1% while in comparable terms, net sales grew by 4.6%

-

Comparable operating profit totalled €102.0 million (€95.6 million), representing an increase of €6.5 million

-

Operating profit totalled €96.6 million (€89.4 million)

-

Cash flow from operating activities totalled €77.7 million (€-24.5 million)

-

Comparable earnings per share €0.14 (€0.13); reported earnings per share €0.13 (€0.12)

> See the Q1/2026 interim report and presentation materials

Recap of Kesko's key events in Q1/2026

Kesko will publish its first-quarter results for 2026 on Wednesday, 29 April 2026, at around 8.00 am Finnish time. An English-language audiocast/teleconference for investors and analysts will be held at 9.00 am Finnish time.

Below is a recap of key events and materials for the quarter from an investor perspective.

NEWS, FINANCIALS AND SHARES

-

Kesko’s Annual General Meeting of shareholders was held on 26 March 2026. The Meeting resolved, among other things, to distribute a dividend of €0.90/share for 2025, and elected 7 members to Kesko’s Board of Directors for a one-year term of office, including Mervi Airaksinen as a new member. (release)

At its organisational meeting, the Board of Directors re-elected Esa Kiiskinen as its Chair. (release)

-

Kesko’s Annual Report for 2025 was published in February. The report comprises a general review of the company’s strategy, businesses and key sustainability efforts and targets, a Corporate Governance Statement and Remuneration Report, as well as the financial statements section, which includes a sustainability statement. (release)

-

Jan-Erik Fredriksson was appointed as Kesko’s new Chief Information Officer (CIO). He comes to Kesko from Fortum, and will assume his position in August 2026 at the latest. (release)

-

Shares:

-

Presentation for Kesko’s Q1 investor roadshow meetings. (presentation)

SALES DEVELOPMENT

Sales figures for March will be released in mid-April.

GROCERY TRADE

-

Efforts to turn around market share development yielded results towards the end of 2025. K Group grocery stores managed to increase their market share by 0.5 percentage points in the final quarter of 2025, and by 0.2 percentage points in July-December 2025. In the hypermarket segment, Kesko’s K-Citymarket chain gained market share throughout last year. In Q4, K Group grocery stores won over market share in all store size segments. The positive development can be attributed to Kesko’s strategic investments in the store network as well as in the quality and price levels of the grocery stores. (release)

In total, Kesko’s grocery trade market share in 2025 amounted to 33.5% according to the Nielsen IQ Grocery Shop Directory. (release)

SUSTAINABILITY

-

SBTi validated Kesko’s new science-based emission reduction targets. The Science Based Targets initiative (SBTi) has validated Kesko’s new near term and long term science-based emission reduction targets, extending to 2034 and 2050, respectively. Kesko is set to reduce emissions from its own operations through, for example, increased use of electric transportation and improved energy efficiency. Emissions from products sold will be reduced in close cooperation with suppliers. (release)

-

Kesko ranks highest in its sector in both the European and global listings of the most sustainable companies. The Canadian media and research organisation Corporate Knights publishes annual listings of the most sustainable companies in the world and in Europe. Kesko ranked the highest of all companies in its sector in both listings this year. Kesko is the only company in the world to have been included in the global sustainability listing every year since it was first launched in 2005. (Europe 50 release, Global 100 release)

President and CEO Rauhala: Kesko's result improved and net sales increased in all divisions in 2025

"Kesko’s comparable operating profit improved and net sales increased in all three divisions in 2025. The full-year net sales amounted to €12,474.1 million and comparable operating profit to €654.9 million. In the latter half of the year, there was a turnaround in profit, as quarter-result improved in Q3 and growth continued in Q4. The successful execution of our updated growth strategy in all divisions has yielded results even in an operating environment that has continued to be challenging. Our cost control has also been effective. Our good ability to generate profit and financial position have enabled investments in growth, and we will continue strong growth investments also in upcoming years. Kesko’s Board of Directors proposes to the Annual General Meeting a dividend payment in line with the company’s dividend policy: €0.90 per share, or over €358 million in total, to be paid in four instalments.

Kesko’s Board proposes a dividend payment of €0.90 per share, over €358 million in total, in line with the company's dividend policy

Net sales for Kesko’s grocery trade division grew and totalled €6,447.7 million in 2025, with a comparable operating profit of €418.1 million.

Kesko’s objective in grocery trade is to strengthen its market position while maintaining good profitability. Both were achieved in 2025. Operating margin for the division stood at 6.5%. The market share development for K Group grocery stores was very close to the market trend for full-year 2025. A significant turn was seen in the summer, and our market share grew by 0.2 percentage points in July-December and by 0.5 percentage points in Q4 (source: Finnish Grocery Trade Association). The K-Citymarket chain gained market share in the hypermarket segment throughout 2025, and in the final quarter, all K Group grocery chains won over market share in their respective segments. Kesko’s strategic investments in the grocery store network and the price and quality levels of the stores are yielding results. The total grocery trade market also grew from the summer onwards. In the foodservice business, Kespro gained market share despite the 0.3% decrease in sales.

In the building and technical trade division, both net sales and comparable operating profit grew despite the weak cycle in new housing construction. Net sales for the division totalled €4,685.8 million, with a comparable operating profit of €178.6 million. The full-year 2025 profit improved in building and home improvement trade and was close to flat in technical trade, while in the final quarter, profit improved in both business areas. We strengthened market position for Davidsen in Denmark by acquiring three local building and home improvement trade operators in 2025: Roslev, Tømmergaarden and CF Petersen & Søn. Kesko’s biggest ever construction project, the joint Onninen and K-Auto logistics centre Onnela in Hyvinkää, Finland, was completed in 2025. Gradual recovery in the construction cycle continued throughout the year, but the pace of recovery in the latter half of the year was weaker than anticipated, especially in new housing construction. In the longer term, however, outlook for the building and technical trade division is positive. Strategic focus for the division is on securing growth and profitability and improving cash flow in each country and business.

Net sales for the car trade division in 2025 increased by 12% and totalled €1,364.8 million, with a comparable operating profit of €83.1 million. The division managed to improve its net sales and comparable operating profit significantly despite the fact that the car trade market in Finland continued to be challenging, as consumer confidence stayed weak and uncertainty regarding powertrain choices persisted. Net sales grew in new and used cars, car services, and sports trade. The strong product and service portfolio and significant transformation measures carried out within the division in recent years have resulted in improved sales and profitability. Kesko’s objective in car trade is to outperform the market in all business areas.

Our market position grew stronger in nearly all business areas in 2025. We estimate that both our operating environment and results will improve in 2026 in all divisions and operating countries. I want to thank all our customers, the people of K Group, our shareholders, and our partners for their trust and cooperation in 2025.

KEY FIGURES IN OCTOBER-DECEMBER 2025:

-

Group net sales in October-December totalled €3,230.9 million (€3,040.6 million); reported net sales grew by 6.3% while comparable net sales grew by 3.1%

-

Comparable operating profit totalled €174.6 million (€170.8 million), representing an increase of €3.8 million

-

Operating profit totalled €160.1 million (€121.0 million)

-

Cash flow from operating activities totalled €292.5 million (€301.0 million)

-

Comparable earnings per share €0.28 (€0.31); reported earnings per share €0.25 (€0.19)

KEY FIGURES IN JANUARY-DECEMBER 2025:

-

Group net sales in January–December totalled €12,474.7 million (€11,920.1 million); reported net sales grew by 4.7%, while comparable net sales grew by 2.3%

-

Comparable operating profit totalled €654.9 million (€650.1 million), representing an increase of €4.8 million

-

Operating profit totalled €631.3 million (€579.5 million)

-

Cash flow from operating activities totalled €879.7 million (€1,008.2 million)

-

Comparable earnings per share €1.07 (€1.11); reported earnings per share €1.02 (€0.95)

> See the full 2025 financial statements release and presentation materials