Investor blogs and podcasts

In Kesko’s investor blogs and podcasts, Kesko’s management discusses topical issues relevant to investors and shareholders.

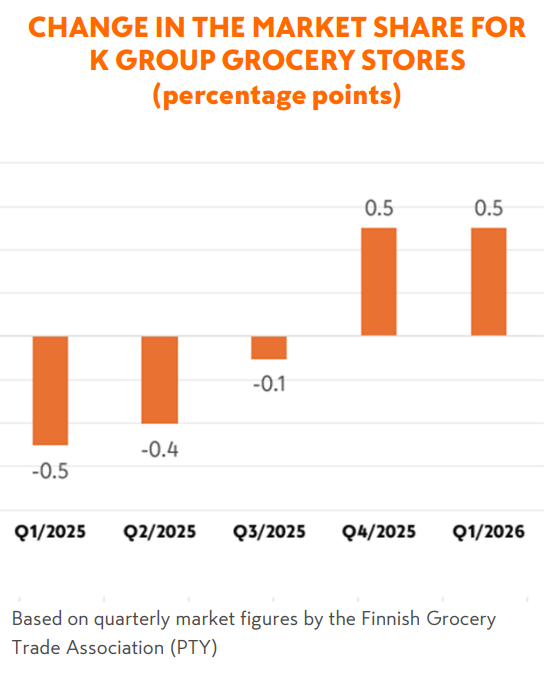

K Group grocery stores are gaining market share while maintaining good profitability

The market share for K Group grocery stores grew by 0.5 percentage points year-on-year in the first quarter of 2026 (source: Finnish Grocery Trade Association, PTY). After negative development in 2022-2024, K Group’s market share took a positive turn last summer, and between October and March we gained market share every month. The K-Citymarket chain gained market share in the hypermarket segment throughout last year. In Q4/2025 and Q1/2026, our other two grocery chains – K-Market and K-Supermarket – also gained market share in their respective segments (in year-on-year comparison). The total grocery market in Finland grew by 2.9% in Q1, while K Group’s grocery sales grew by 4.4%.

Strengthening market share was one of the main objectives set for Kesko’s grocery trade division when the Group strategy was updated in spring 2024. However, it was equally important to maintain good profitability despite efforts to boost market share, and the division’s operating margin target was set at “clearly above 6%”. In the first quarter of 2026, the division’s operating margin was strong at 6.5% (rolling 12 months) despite the market share gains achieved.

Investments in quality, prices and store network development contributing to market share growth

The positive development in market share can be attributed to the long-term strategic investments made in the price and quality levels of the stores as well as the development of the grocery store network.

Prices: The Finnish grocery trade market has been very price-driven in recent years, and price continues to be an important consideration for many customers. In January 2025, Kesko and K-retailers launched an extensive long-term price programme, cutting prices on more than 1,200 popular everyday staples in K Group grocery stores. Combined, Kesko and the retailers invested €50 million in the programme last year. In addition to the price programme, we have actively invested in campaigns as well as in targeted personal offers and benefits. The efforts have paid off, as customer flows in K Group grocery stores have grown. Average purchase is also up, and customers are not buying only the discounted products, but increasingly do their main weekly shop at our stores.

Quality: Raising the quality level of K Group grocery stores further involves a wide range of actions aiming to ensure suitable selections, good product availability, excellent customer service, reliable and useful digital services, and high quality products. In the current strategy period, special attention has been paid to certain key product categories, such as bread and fruit and vegetables. The implementation of store-specific business ideas, tailored to local demand and customer base, plays a crucial role in developing better stores. The business ideas can be implemented even more effectively with the help of new tools that utilise data and AI for easier selection and campaign management, thus freeing up store staff for more personal customer service.

Efforts to improve quality have paid off, as customer satisfaction grew clearly in all three K Group grocery chains in both Q4/2025 and Q1/2026. Demand for valuable and premium product categories, such as service counter items, fruit and vegetables and high-quality ready meals, has also grown.

New premium flower departments and the development of popular K-Ruoka digital services are examples of investments made in customer service and quality.

Store network: Having the right-sized stores situated in the right locations supports positive market share development. Kesko invests €200-250 million annually in the development of its grocery store network. In 2025, we opened 60 new or remodelled stores, including 2 new K-Citymarket hypermarkets. In 2026, we will open 25 new stores and remodel more than 60. Network development covers stores of all sizes, although growth in Finnish grocery trade in recent years has been the strongest in larger stores sizes, such as hypermarkets. In new store openings, our focus is especially on urban growth centres. Meanwhile, store remodelling often involves aspects such as updating refrigeration equipment to meet the requirements of tightening EU regulations.

Network development can also involve closing stores, which can have a negative market share impact in the short term. For example, the discontinuation of the Neste K chain in 2024 reduced the number of our stores by over 60. All together, network changes made by both K Group and its competitors had a negative impact on K Group’s market share in 2025, while in 2026, the impact is expected to be neutral. Network development efforts should gradually support our market share development in upcoming years.